The following data were extracted from the accounting records of Harkins Company for the year ended April 30, 2019:

Increase in estimated returns inventory $ 11,600

Merchandise inventory, May 1, 2018 380,000

Merchandise inventory, April 30, 2019 415,000

Purchases 3,800,000

Purchases returns and allowances 150,000

Purchases discounts 80,000

Sales 5,850,000

Freight in 16,600

a. Prepare the cost of merchandise sold section of the income statement for the year ended April 30, 2019, using the periodic inventory system.

b. Determine the gross profit to be reported on the income statement for the year ended April 30, 2019.

c. Would gross profit be different if the perpetual inventory system was used instead of the periodic inventory system?

Answer:

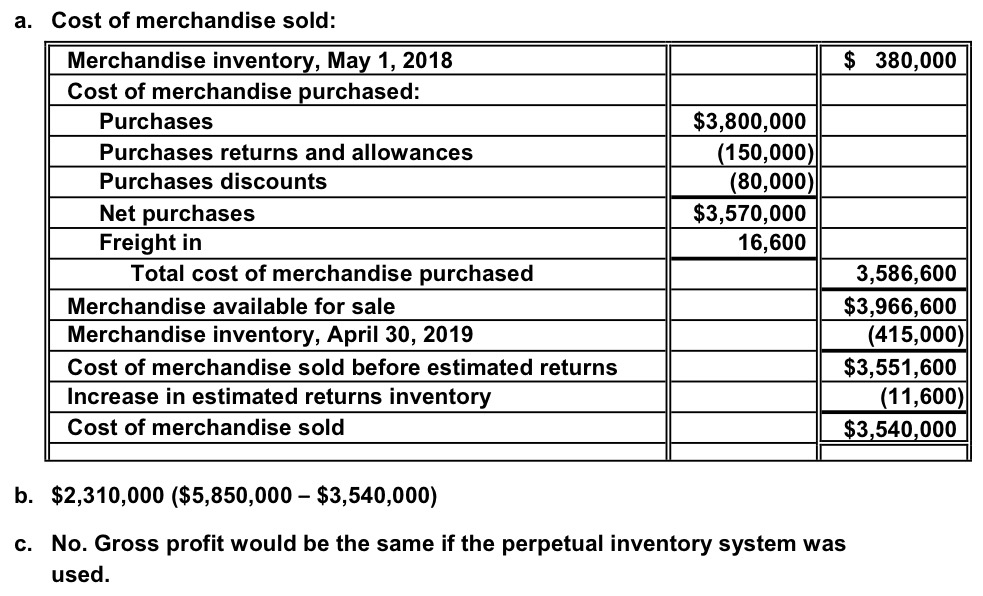

a. Cost of merchandise sold:

Merchandise inventory, May 1, 2018$ 380,000

Cost of merchandise purchased:

Purchases$3,800,000

Purchases returns and allowances (150,000)

Purchases discounts(80,000)

Net purchases$3,570,000

Freight in16,600

Total cost of merchandise purchased 3,586,600

Merchandise available for sale$3,966,600

Merchandise inventory, April 30, 2019(415,000)

Cost of merchandise sold before estimated returns $3,551,600

Increase in estimated returns inventory(11,600)

Cost of merchandise sold$3,540,000

b. $2,310,000 ($5,850,000 – $3,540,000)

c. No. Gross profit would be the same if the perpetual inventory system was

used.